Staying ahead of global payment regulations is a constant challenge for CISOs and compliance officers. PCI certification is more than a checklist—it serves as proof your team has implemented robust security controls to protect cardholder data. Understanding certification levels, validation requirements, and assessor roles helps you target resources where they matter most, minimize audit stress, and build trust with clients and partners.

Table of Contents

- PCI Compliance Certifications Explained Clearly

- Types of PCI Compliance Levels and Standards

- Certification Process and Verification Steps

- Legal Requirements and Industry Obligations

- Risks, Costs, and Common Pitfalls

Key Takeaways

| Point | Details |

|---|---|

| Understand PCI Levels | Organizations must identify their PCI compliance level based on annual transaction volume, as it determines assessment requirements and operational burden. |

| Continuous Compliance | PCI compliance is not a one-time event; regular validation and maintenance of security controls are essential to remain compliant and mitigate risks. |

| Engage Qualified Assessors | Employing qualified assessors is crucial for accurate audits and ensuring compliance with PCI DSS, especially for Level 1 merchants undertaking on-site evaluations. |

| Document Thoroughly | Accurate documentation of security controls and compliance efforts is vital to prove adherence during assessments and protect against potential liability. |

PCI Compliance Certifications Explained Clearly

PCI compliance certifications validate that your organization meets baseline security standards for handling payment card data. These certifications aren't optional for most businesses—they're mandatory if you accept, store, or transmit cardholder information. Understanding what they actually mean helps you allocate resources effectively and reduce audit friction.

The foundation starts with PCI DSS compliance, a security standard created by major credit card companies. It's not a single checkbox but rather a comprehensive framework covering data protection during storage, processing, and transmission. Think of it as the baseline security language that payment processors, acquirers, and card networks all speak.

Four Levels of Certification

Your organization falls into one of four compliance levels based on annual payment card transaction volume. This level determines your assessment requirements and reporting burden.

- Level 1: Over 6 million transactions annually—requires annual assessments by qualified auditors and quarterly vulnerability scans

- Level 2: 1 to 6 million transactions—annual self-assessment questionnaire with quarterly scans required

- Level 3: 20,000 to 1 million online transactions—self-assessment questionnaire and quarterly scans

- Level 4: Fewer than 20,000 online transactions—self-assessment questionnaire option available

Higher transaction volumes mean stricter validation requirements. A Level 1 merchant faces significantly more rigorous assessments than a Level 4 merchant, which affects timeline and resource investment.

What Certification Actually Proves

When your organization receives PCI certification, you're demonstrating concrete security controls. These include firewalls, anti-virus protection, encryption for cardholder data, access controls, and regular security testing. Certification proves these controls exist and function correctly, not just that you claim they do.

This matters operationally. Partners, clients, and payment processors trust certified organizations more. Breach risk drops significantly when controls are validated. You're also reducing theft and fraud exposure that could devastate revenue and reputation.

The Role of Assessors and Training

The PCI Security Standards Council qualifies individuals and organizations who validate compliance. These qualified assessors conduct audits, review security documentation, and issue official compliance reports. Their credentials matter—they've passed Council testing and understand PCI requirements deeply.

You'll encounter two types of professionals:

- Qualified Security Assessors (QSAs) conduct on-site audits for larger merchants

- Internal Security Assessors (ISAs) validate compliance for qualifying organizations

Both roles require specific training and annual maintenance. This professionalization ensures assessments meet consistent standards globally.

Certification validity typically lasts one year, meaning your compliance posture requires continuous attention—not a one-time achievement.

Pro tip: Don't wait until renewal time to address compliance gaps. CISOs who embed quarterly PCI validation checks into their security calendar catch issues early and reduce audit surprises.

Types of PCI Compliance Levels and Standards

PCI compliance isn't one-size-fits-all. The Payment Card Industry divides requirements into four distinct levels based on your transaction volume. Your assigned level determines audit frequency, assessment type, and overall compliance burden.

This structure makes sense operationally. A merchant processing 50 million transactions annually faces different risks than one processing 100,000. The framework scales validation requirements proportionally, preventing smaller merchants from drowning in unnecessary overhead.

Understanding the Four Levels

PCI compliance levels are determined by your annual credit card transaction volume. Each level carries specific validation and documentation requirements.

- Level 1: Over 6 million transactions yearly—requires annual on-site audits by Qualified Security Assessors, quarterly vulnerability scans, and comprehensive documentation

- Level 2: 1 to 6 million transactions—requires annual self-assessment questionnaire completion and quarterly external vulnerability scans

- Level 3: 20,000 to 1 million online transactions—requires annual self-assessment questionnaire with quarterly scans

- Level 4: Fewer than 20,000 online transactions—may qualify for self-assessment questionnaire option with less frequent scanning

Level 1 merchants face the heaviest lift. The on-site audit requirement means a qualified assessor evaluates your entire cardholder data environment directly. Levels 2 through 4 use self-assessment questionnaires, which reduce assessment cost but require your team to accurately document controls.

Here's a comparison of the four PCI compliance levels and their operational impact:

| PCI Level | Audit Requirement | Operational Impact | Typical Organization |

|---|---|---|---|

| Level 1 | On-site by QSA | High labor, high cost | Large retailers, processors |

| Level 2 | Self-assessment + scans | Moderate labor, moderate cost | Medium-sized businesses |

| Level 3 | Self-assessment + scans | Lower labor, less complexity | E-commerce SMBs |

| Level 4 | Optional self-assessment | Minimal labor, lowest cost | Small local merchants |

Beyond Transaction-Based Levels

The PCI Data Security Standard itself is the foundational framework all merchants follow. Beyond DSS, the Council maintains additional standards addressing specific security domains.

- Point-to-Point Encryption (P2PE): Protects card data during transmission through encrypted channels

- Payment Application Data Security Standard (PA-DSS): Ensures software vendors build secure payment applications

- PCI Software Security Framework: Guides secure development practices for payment software

- Tokenization standards: Define secure data substitution methods

Your organization might comply with multiple standards simultaneously. A payment processor handling Level 1 transaction volume likely follows DSS requirements plus PA-DSS for applications they develop. This layered approach strengthens overall security posture.

Validation Requirements by Level

Each level specifies distinct validation approaches. Level 1 merchants cannot self-assess; they need independent verification. Levels 2-4 gain flexibility in how they prove compliance, though external scanning remains mandatory.

The frequency matters too. Level 1 requires continuous validation attention. Levels 3 and 4 might complete assessments annually with less operational interruption.

Your compliance level can change if transaction volume shifts—monitor this annually to avoid unexpected assessment requirements.

Pro tip: Map your transaction volume trajectory for the next 24 months. If you're approaching a level threshold, begin implementing that level's requirements early rather than scrambling after recategorization.

Certification Process and Verification Steps

Getting PCI certified isn't automatic. It requires deliberate steps, documentation, and validation from qualified assessors or your own team, depending on your level. The process demands accuracy and completeness—half-measures won't pass verification.

Your compliance journey starts with understanding where you stand. CISOs must inventory cardholder data flows, identify systems handling sensitive information, and map existing security controls. This baseline assessment determines which PCI requirements apply to your environment.

Step 1: Conduct a Gap Assessment

Before formal audit, determine what you're missing. A gap assessment compares your current security posture against PCI DSS requirements.

- Map all systems storing or transmitting cardholder data

- Document existing firewalls, encryption, access controls, and monitoring

- Identify missing controls or weak implementations

- Prioritize remediation based on risk and complexity

This isn't optional. Level 1 merchants conducting formal audits will face these questions anyway. Smaller merchants benefit from finding gaps early rather than during verification.

Step 2: Implement Required Controls

Identified gaps require remediation. Implementation timelines vary by complexity. A firewall upgrade might take weeks; establishing comprehensive access controls could span months.

Focus on the 12 PCI DSS requirements:

- Secure network infrastructure

- Protect cardholder data

- Maintain vulnerability management

- Implement access controls

- Monitor and test networks regularly

- Maintain security policies

Each requirement contains specific controls. Level 1 merchants cannot skip any; Levels 2-4 may focus on requirements matching their environment.

Step 3: Documentation and Evidence Gathering

Verification requires proof. You'll need comprehensive documentation showing each control exists and functions.

- Network diagrams showing data flows

- Encryption certificates and key management procedures

- Access control lists and user privilege reviews

- Firewall rules and logging configurations

- Vulnerability scan reports and remediation records

- Security policy documents and training records

This is where many organizations stumble. Control implementation and control documentation are two different challenges. A firewall exists, but do you have current firewall logs? An access review happened, but did you document findings?

Step 4: Vulnerability Scanning

All PCI levels require external vulnerability scanning from approved scanning vendors. These automated scans test your systems from outside your network, detecting exposed vulnerabilities.

Quarterly scans are mandatory. After remediation, you'll run scans again to confirm vulnerabilities are closed. Passed scans mean "no critical vulnerabilities detected"—not zero vulnerabilities, but none rated critical or high severity.

Step 5: Formal Assessment

Level 1 merchants face on-site audits by Qualified Security Assessors. The assessor reviews documentation, tests controls, interviews staff, and validates compliance.

Levels 2-4 complete self-assessment questionnaires (SAQs). You answer detailed questions about your environment and controls, then submit attestations confirming accuracy.

Formal assessment is verification by definition—passing proves you've met requirements at that point in time.

Step 6: Remediation and Revalidation

Assessments often identify findings. Minor findings require remediation before certification. You'll implement fixes, gather evidence, and revalidate.

This cycle continues annually. Compliance is not permanent; it's a continuous cycle of validation, monitoring, and improvement.

Pro tip: Implement a compliance checklist using a structured framework that maps to your specific PCI level. Organizations using documented checklists complete assessments 40% faster than those managing compliance informally.

Legal Requirements and Industry Obligations

PCI compliance isn't optional. It's contractually mandatory for any business accepting payment cards. You don't comply because federal law requires it; you comply because your payment processor, acquiring bank, and card networks demand it in writing.

This distinction matters legally. Non-compliance doesn't violate federal statute, but it violates your merchant agreement. That contract breach carries teeth—fines, account termination, and liability in data breach lawsuits.

The Contractual Nature of PCI

PCI DSS is not a law but rather an industry standard enforced through contracts. Visa, Mastercard, American Express, and Discover require compliance as a condition of payment processing.

Your merchant agreement explicitly references PCI DSS. By accepting card payments, you've contractually agreed to meet PCI standards. Failure constitutes breach of contract, giving payment processors grounds to:

- Suspend payment processing privileges

- Impose monthly fines or penalties

- Increase processing fees significantly

- Terminate merchant accounts entirely

Larger merchants understand this. Smaller merchants sometimes treat PCI as optional guidance rather than contractual obligation. That misunderstanding becomes expensive fast.

State Data Protection Laws

While PCI DSS itself isn't federal law, many state data protection statutes create overlapping legal obligations. California's Consumer Privacy Act, New York's SHIELD Act, and similar regulations require businesses to protect consumer data or face statutory damages.

Data breaches exposing cardholder information trigger these laws. If you're not PCI compliant and experience a breach, you face both:

- Civil liability under state data protection laws

- Regulatory enforcement actions

- Class action lawsuits from affected consumers

Compliance with PCI DSS generally satisfies many state requirements because PCI standards exceed baseline state obligations.

Breach Liability and Financial Exposure

Non-compliance amplifies breach consequences. If attackers compromise unencrypted cardholder data in a non-compliant environment, liability becomes catastrophic.

Payment processors conduct breach investigations. They determine whether the merchant was PCI compliant when the breach occurred. Compliant merchants often have payment processor indemnification. Non-compliant merchants typically bear full liability costs:

- Card reissuance costs (often $5-$15 per compromised card)

- Forensic investigation expenses

- Notification and credit monitoring services

- Regulatory fines and penalties

- Class action settlement costs

A breach affecting 10,000 cardholders costs $50,000 to $150,000 minimum in reissuance alone. Non-compliance often multiplies this through regulatory penalties.

Industry Enforcement and Professional Certifications

Professional certifications demonstrate your organization takes compliance seriously. The PCI Security Standards Council qualifies assessors, auditors, and compliance professionals.

These certifications matter contractually. Payment processors often require:

- Assessments by Council-qualified professionals

- Annual training for staff handling cardholder data

- Documentation of compliance efforts

Certified professionals validate your compliance claims credibly, strengthening your position in breach disputes or regulatory inquiries.

Your compliance obligation is continuous. Annual certification proves you met requirements at that moment—you must maintain standards year-round.

Pro tip: Document your PCI compliance journey comprehensively. Maintain records of assessments, remediation efforts, policy updates, and staff training. This documentation proves good faith compliance efforts if a breach occurs, potentially limiting liability exposure.

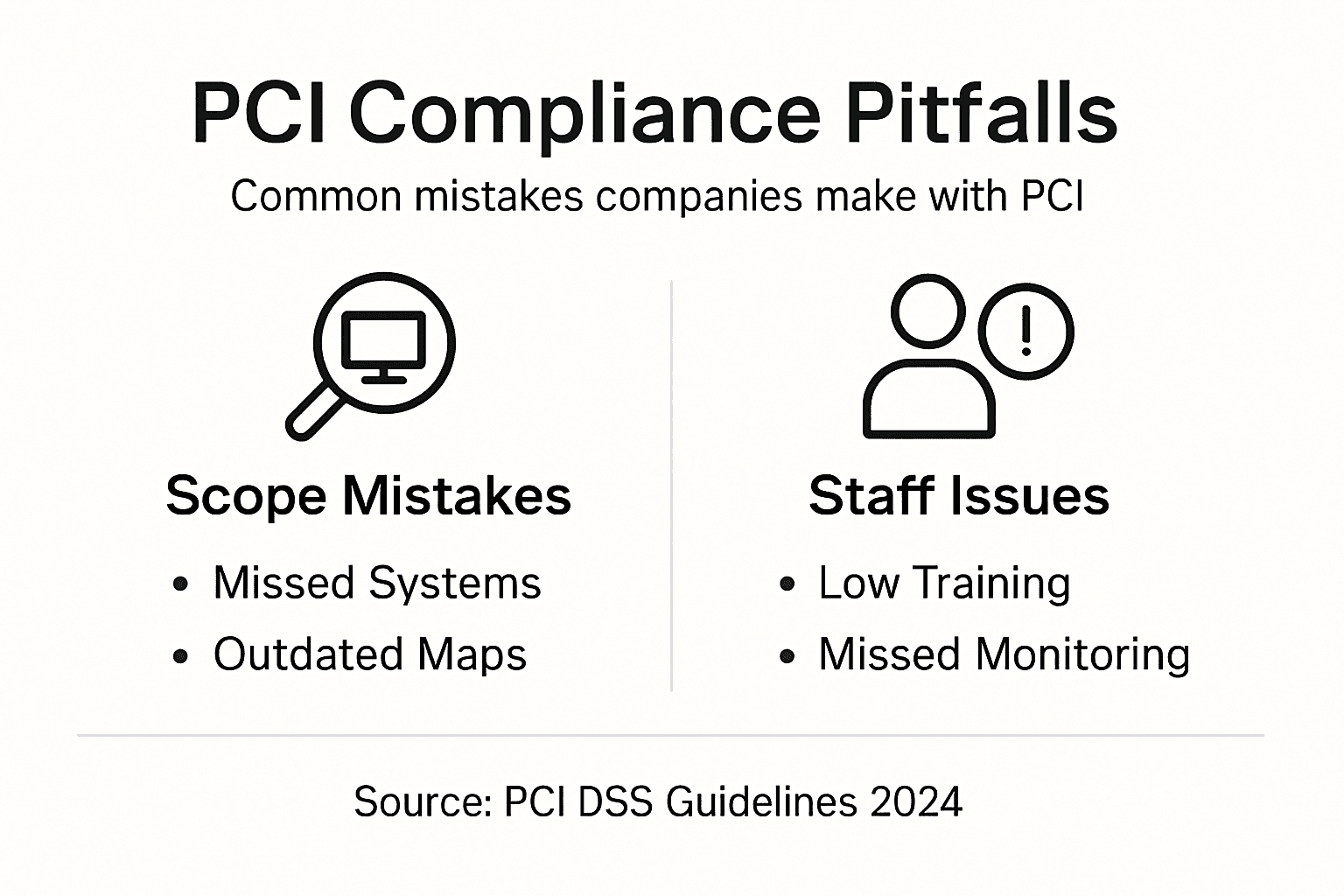

Risks, Costs, and Common Pitfalls

PCI compliance requires real investment. Many organizations underestimate both the financial commitment and the operational complexity required to achieve and maintain certification. That miscalculation creates expensive problems downstream.

Costs vary dramatically by organization size and existing infrastructure maturity. Small businesses might spend under $30,000 annually; larger enterprises invest hundreds of thousands or millions. The variation depends on where you're starting from and how much technical debt you carry.

Understanding True Compliance Costs

PCI compliance costs span multiple categories, not just audit fees. Most organizations miss hidden expenses until budgeting time arrives.

Typical cost components include:

- Infrastructure upgrades (firewalls, encryption, network segmentation)

- Qualified assessor or auditor fees ($10,000-$50,000+ for Level 1)

- Vulnerability scanning services (quarterly, $2,000-$5,000 annually)

- Staff training and education programs

- Documentation and policy development

- Remediation and ongoing security improvements

- Incident response planning and testing

A single Level 1 audit often costs $50,000-$100,000. Add infrastructure improvements, and the first-year investment easily exceeds $200,000. Ongoing annual costs stay substantial, even post-implementation.

The following table summarizes key hidden PCI compliance cost drivers:

| Cost Driver | Why It's Significant | Typical Annual Outlay |

|---|---|---|

| Infrastructure Upgrades | Required for baseline security | $10,000-$100,000 |

| Assessor Fees | Essential for Level 1 audit | $10,000-$50,000 |

| Staff Training | Ensures ongoing compliance | $2,000-$10,000 |

| Vulnerability Scanning | Must be performed quarterly | $2,000-$5,000 |

The One-Time Project Trap

Many organizations treat PCI compliance as a one-time checkbox. You get certified, check the box, move on. That approach guarantees failure.

Compliance is continuous. Controls degrade over time. Staff turnover means new people don't understand security protocols. Technology changes create new vulnerabilities. Treating certification as ongoing rather than a one-time event is essential.

Organizations that succeed view compliance as a permanent operational discipline, not a project with an end date. This mindset shift requires:

- Quarterly compliance reviews

- Regular staff training refreshes

- Continuous monitoring and testing

- Annual reassessment and recertification

- Rapid response to control failures

Common Pitfalls That Lead to Failure

CISOs and compliance officers repeatedly encounter the same mistakes. Learning from them saves time and money.

Underestimating scope: Many organizations misdefine their cardholder data environment. They miss systems touching card data, leading to incomplete assessments and failed audits.

Insufficient staff training: Compliance requires people who understand the requirements. Underfunded training programs mean staff don't grasp their responsibilities, creating control failures.

Ignoring continuous monitoring: After certification, organizations stop monitoring. Networks change, vulnerabilities emerge, and controls fail silently. Then audit time arrives and findings multiply.

Inadequate documentation: Controls exist, but nobody documented them. Assessors can't verify what wasn't recorded. Assessment delays and failed audits follow.

Outdated requirements awareness: PCI DSS evolves. Organizations still following version 3.2 standards face version 4.0 requirements. That disconnect creates audit findings and remediation work.

Breach Risk and Financial Exposure

Non-compliance dramatically increases breach severity. A breach at a compliant organization causes less damage than one at a non-compliant organization with the same attack vector.

Compliance means encryption, access controls, monitoring, and incident response planning actually work. Non-compliance means attackers move freely and damage spreads widely. The financial consequences are brutal: forensics, notification, credit monitoring, regulatory fines, and litigation costs.

One major breach can cost millions. Compliance investment looks inexpensive by comparison.

Pro tip: Budget for continuous compliance from year one. Set aside 15-20% of your initial compliance investment annually for ongoing maintenance, training, and improvements. Organizations treating compliance as a continuous operational cost outperform those trying to minimize year-to-year spending.

Accelerate Your PCI Compliance Certification with Skypher's AI-Powered Automation

PCI Compliance Certifications demand rigorous documentation, continuous validation, and precise responses to complex security questionnaires. Organizations face challenges such as managing large volumes of audit questions accurately and maintaining up-to-date evidence to prove their security controls function correctly. Skypher solves these obstacles by offering an AI Questionnaire Automation Tool that streamlines your entire compliance process. With intelligent parsing of all questionnaire formats and integrations with over 30 third-party risk management platforms, you can drastically reduce the time spent on PCI DSS self-assessment questionnaires and audits.

Take control of your PCI compliance journey today with Skypher. Benefit from real-time collaboration features, seamless integrations with tools like ServiceNow and Slack, and AI-driven accuracy that boosts your cybersecurity efficiency. Whether you are a Level 1 merchant facing on-site audits or a smaller organization completing SAQs, Skypher helps you manage continuous compliance confidently and avoid costly pitfalls. Discover how to optimize your security questionnaire workflows now by exploring our comprehensive platform at Skypher's landing page.

Frequently Asked Questions

What is PCI Compliance Certification?

PCI Compliance Certification validates that an organization meets security standards for handling payment card data. It is essential for any business that accepts, stores, or transmits cardholder information.

What are the different levels of PCI Compliance?

PCI Compliance is categorized into four levels based on annual transaction volume. Level 1 is for those processing over 6 million transactions, requiring the most stringent assessments, while Level 4 is for those with fewer than 20,000 transactions and has less rigorous requirements.

How often do companies need to validate PCI Compliance?

Certification validity typically lasts one year, and companies must undergo continuous monitoring and regular assessments to maintain compliance, especially as transaction volumes change.

What is the importance of hiring qualified assessors for PCI compliance?

Qualified assessors conduct thorough audits and validations, ensuring that organizations meet PCI DSS requirements. Their expertise helps identify security gaps and improves trust with partners and clients.

Recommended

- Compliance Risk Meaning: Impact on Security Reviews

- ISO 27001: Impact on Tech Security Compliance

- Automated Compliance: Transforming Security Reviews

- Complete Guide to Software Compliance Software

- Industry Accreditation in Security – Why It Matters

- Infrastructure Automation & DevSecOps – IronByte Consulting and Training

- Website Security and Data Protection Services | Brainiac Media