Complex security questionnaires often stall when teams encounter uncertainty around internal financial controls. For compliance officers and risk managers at global tech and finance firms, understanding a SOC 1 report is vital for vetting third-party providers handling payroll, accounting, or transaction processing. By clarifying common misconceptions and showing real SOC 1 report examples, this guide helps you address financial reporting risks and strengthen your organization's due diligence.

Table of Contents

- Defining SOC 1 Reports And Common Misconceptions

- Types Of SOC 1 Reports: Type I Vs. Type II

- Key Components In A SOC 1 Report Example

- SOC 1 Report Requirements And Compliance Steps

- Risks, Challenges, And Best Practices For Firms

Key Takeaways

| Point | Details |

|---|---|

| Understanding SOC 1 Reports | SOC 1 reports evaluate a service organization's internal financial controls, vital for businesses using third-party services. |

| Types of SOC 1 Reports | Type I assesses design at a point in time, while Type II evaluates operational effectiveness over a period, typically 6-12 months. |

| Key Components of SOC 1 Reports | Important elements include the auditor's opinion, management assertion, and control testing results, all crucial for trust and transparency. |

| SOC 1 Compliance Steps | Organizations must identify control objectives, develop documentation, and engage in robust testing to achieve compliance effectively. |

Defining SOC 1 Reports and Common Misconceptions

A SOC 1 report is a specialized audit assessment that evaluates an organization's internal financial controls and reporting processes. These independent evaluations are critical for businesses that rely on third-party service providers for financial operations like payroll, accounting, or transaction processing. Understanding SOC reporting standards helps organizations maintain robust financial integrity and transparency.

Unlike broader security assessments, SOC 1 reports have a laser-focused objective: confirming that a service organization's controls will not negatively impact their clients' financial statements. The reports come in two primary types:

- Type I: Assesses the design of control systems at a specific point in time

- Type II: Evaluates the operational effectiveness of these controls over a defined period (typically 6-12 months)

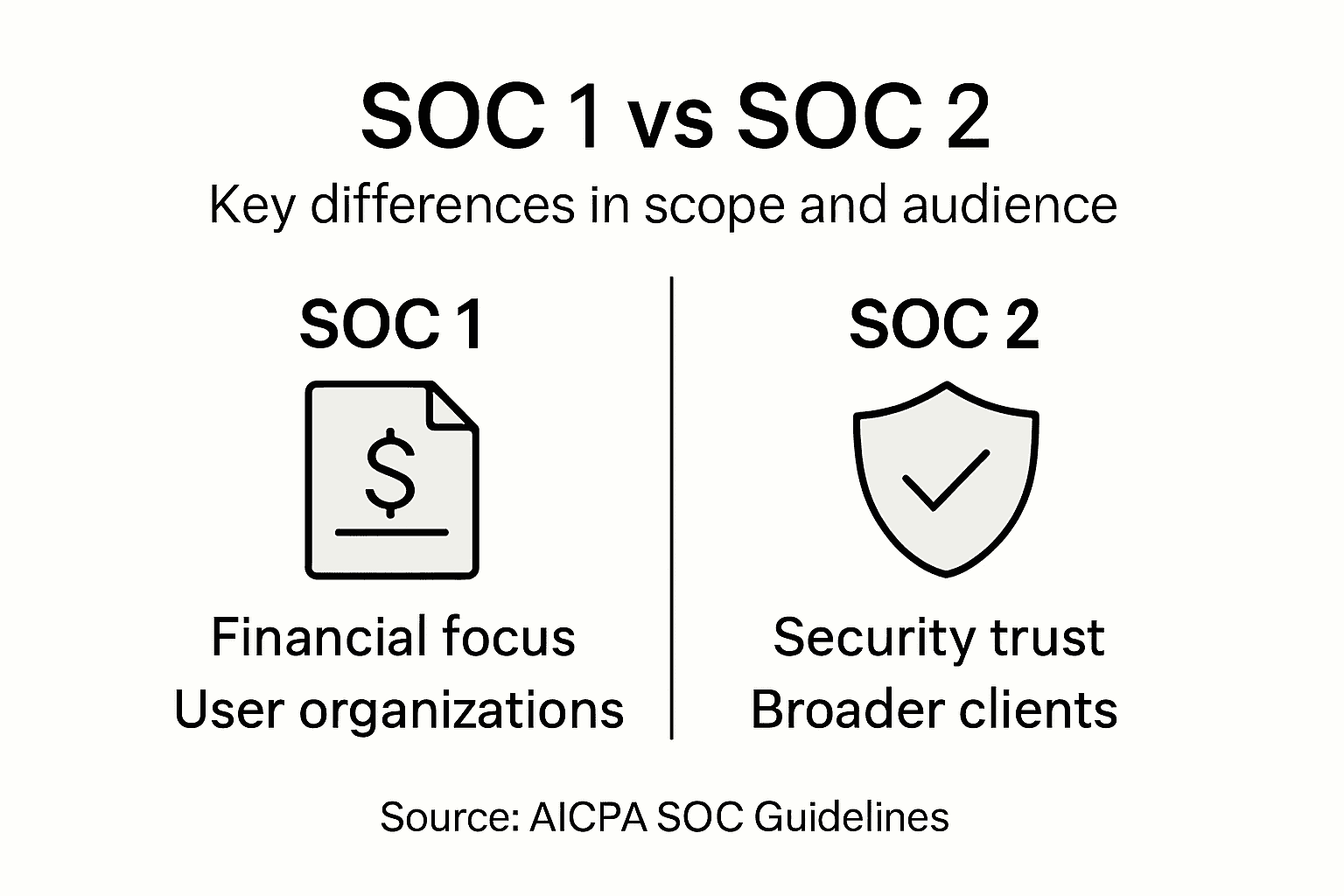

Common misconceptions about SOC 1 reports can lead to significant misunderstandings. Many professionals mistakenly believe SOC 1 is equivalent to SOC 2 or a formal certification, which is incorrect. SOC 1 is specifically tailored for financial reporting controls, targeting financial auditors and stakeholders directly involved in financial processes.

The key difference between SOC 1 and other SOC reports lies in their scope and audience. While SOC 2 focuses on broader trust service criteria like security, availability, and privacy, SOC 1 remains narrowly concentrated on financial reporting controls. This specialized approach allows for a more precise evaluation of potential financial risks and control mechanisms.

The following table highlights how SOC 1, SOC 2, and SOC 3 reports differ in focus, audience, and reporting details:

| Report Type | Primary Focus | Intended Audience | Reporting Detail |

|---|---|---|---|

| SOC 1 | Financial controls | Auditors, finance stakeholders | Controls affecting financial statements |

| SOC 2 | Trust criteria (security, availability, privacy) | Management, clients, regulators | Security and operational controls |

| SOC 3 | Broad trust criteria summary | Public, clients | General overview, not detailed |

Pro tip: When requesting a SOC 1 report, clearly specify whether you need a Type I or Type II assessment to ensure you receive the most relevant financial control information.

Types of SOC 1 Reports: Type I vs. Type II

Companies seeking comprehensive financial control assessments must understand the critical differences between SOC 1 Type I and Type II reports. SOC report types provide distinct levels of assurance for organizations evaluating their internal financial control mechanisms.

SOC 1 Type I reports focus on a specific moment in time, offering a snapshot of an organization's control design and implementation. Key characteristics include:

- Evaluates control system design at a single point

- Provides initial assessment of control framework

- Useful for organizations establishing new financial processes

- Offers limited temporal perspective

In contrast, SOC 1 Type II reports deliver a more comprehensive evaluation by examining both control design and operational effectiveness over an extended period. These reports typically cover a six to twelve-month timeframe and provide deeper insights into an organization's financial control sustainability.

Type II reports represent a more rigorous assessment, demonstrating not just how controls are designed, but how consistently they function over time.

The primary distinctions between Type I and Type II reports center on depth of analysis and duration of assessment. While Type I reports represent a momentary glimpse of control structures, Type II reports validate ongoing control effectiveness, giving stakeholders greater confidence in an organization's financial reporting mechanisms.

Pro tip: When selecting between Type I and Type II reports, consider your organization's maturity and the level of assurance required by your stakeholders.

Key Components in a SOC 1 Report Example

A comprehensive SOC 1 report serves as a critical document for organizations seeking to demonstrate the reliability of their financial control mechanisms. SOC 1 report components provide a detailed framework for evaluating an organization's internal financial reporting controls.

The key components of a SOC 1 report typically include five essential elements:

- Service Auditor's Opinion: An independent assessment of control effectiveness

- Management Assertion: The service organization's statement about its control framework

- System Narrative: Detailed description of organizational systems and processes

- Control Testing Results: Comprehensive evaluation of control implementation

- Additional Information: Supplementary details, including potential control deficiencies

The service auditor's opinion represents the most critical component, providing an objective evaluation of the organization's financial control environment.

Detailed control testing validates the organization's financial reporting mechanisms, offering stakeholders a transparent view of internal control effectiveness. Each component plays a crucial role in building trust and providing assurance to clients, investors, and regulatory bodies. The system narrative, in particular, offers in-depth insights into the organization's control objectives, helping stakeholders understand the comprehensive approach to financial risk management.

This table summarizes the business impact of key SOC 1 report components:

| Component | Business Impact | Example Value |

|---|---|---|

| Auditor's Opinion | Builds trust for clients | Increases deal confidence |

| Management Assertion | Shows internal accountability | Demonstrates governance commitment |

| System Narrative | Enhances transparency | Clarifies risk management processes |

| Control Testing Results | Validates ongoing effectiveness | Identifies improvement areas |

| Additional Information | Addresses unique risks | Highlights exceptions or gaps |

Pro tip: Review each section of the SOC 1 report carefully, paying special attention to the auditor's opinion and control testing results to gain a comprehensive understanding of the organization's financial control landscape.

SOC 1 Report Requirements and Compliance Steps

Navigating the SOC 1 compliance process requires a systematic approach to demonstrating financial control effectiveness. Understanding SOC 1 compliance fundamentals helps organizations prepare comprehensive and credible financial reporting controls.

Organizations seeking SOC 1 compliance must follow several critical steps:

-

Identify Relevant Control Objectives

- Determine financial reporting processes requiring assessment

- Map internal controls specific to these processes

- Establish clear documentation of control mechanisms

-

Develop Comprehensive Control Documentation

- Create detailed descriptions of control activities

- Document how controls mitigate potential financial risks

- Ensure traceability and transparency in control design

-

Implement Robust Control Testing

- Design internal testing protocols

- Conduct thorough operational effectiveness evaluations

- Maintain consistent monitoring and assessment processes

Successful SOC 1 compliance requires a proactive approach to documenting, testing, and continuously improving financial control mechanisms.

The compliance journey involves engaging an independent service auditor who will assess the organization's control framework. This professional will review documentation, test control effectiveness, and ultimately provide an objective opinion on the organization's financial reporting controls.

Pro tip: Treat SOC 1 compliance as an ongoing process of continuous improvement, not just a one-time audit requirement.

Risks, Challenges, and Best Practices for Firms

Successful SOC 1 compliance demands a strategic approach to managing potential risks and challenges in financial reporting control environments. Identifying common audit pitfalls helps organizations develop robust risk mitigation strategies.

Key risks and challenges in SOC 1 reporting include:

- Documentation Gaps: Insufficient or unclear control documentation

- Accountability Issues: Undefined roles and responsibilities

- Compliance Complexity: Navigating evolving regulatory requirements

- Audit Readiness: Inadequate preparation for comprehensive assessments

Proactive risk management transforms potential compliance obstacles into opportunities for strengthening organizational control frameworks.

High-quality SOC audits demand strategic approaches to mitigate operational and reputational risks. Best practices for firms include:

-

Conduct Early Readiness Assessments

- Perform comprehensive internal control evaluations

- Identify potential compliance gaps

- Develop targeted improvement strategies

-

Maintain Detailed Documentation

- Create clear, traceable control descriptions

- Establish robust evidence collection processes

- Ensure transparency in control mechanisms

-

Leverage Technological Solutions

- Implement automated control monitoring

- Use advanced analytics for continuous improvement

- Integrate technology-driven compliance tools

Pro tip: Treat SOC 1 compliance as a continuous improvement journey, not a one-time checkbox exercise.

Simplify Your SOC 1 Reporting with AI-Powered Automation

Accurately managing SOC 1 reports demands clear control documentation, efficient testing, and continuous compliance monitoring. This process can be overwhelming for tech and finance organizations facing growing complexity and tight deadlines. Skypher understands your need to boost trust in tech compliance while saving precious time and resources. Our AI Questionnaire Automation Tool helps you respond to security questionnaires faster and with greater accuracy. Key benefits include:

- Rapid handling of complex financial and control-related queries

- Seamless integration with over 40 third-party risk management platforms

- Real-time collaboration features to unify teams and reduce errors

Discover how Skypher’s customizable Trust Center and advanced AI-driven solutions optimize your SOC 1 compliance workflow and increase confidence with clients and auditors alike. Take control of your compliance challenges today and transform SOC 1 reporting from a burden into a competitive advantage. Explore the power of automation at Skypher and learn more about our innovative AI Questionnaire Automation Tool. Get started now for faster, smarter compliance solutions.

Frequently Asked Questions

What is a SOC 1 report?

A SOC 1 report is an independent audit assessment that evaluates an organization's internal financial controls and reporting processes, crucial for businesses that rely on third-party service providers for financial operations.

What are the types of SOC 1 reports?

There are two primary types of SOC 1 reports: Type I, which assesses the design of control systems at a specific point in time, and Type II, which evaluates the operational effectiveness of those controls over a defined period (typically 6-12 months).

How do I choose between SOC 1 Type I and Type II reports?

Select SOC 1 Type I if you need a snapshot of control design for new financial processes. Choose Type II for a comprehensive evaluation of control effectiveness over an extended period, providing deeper insights for stakeholders.

What are the key components of a SOC 1 report?

A SOC 1 report typically includes the Service Auditor's Opinion, Management Assertion, System Narrative, Control Testing Results, and Additional Information that collectively demonstrate the reliability of the financial controls.